An investment in knowledge pays the best interest.

— Benjamin Franklin

Hi everyone! Thanks for stopping by. This is a new venture for me and one that I’ll be refining as I go. My goal is to share with you some of the basics of finance, clear the air on topics you may see in the news from time to time, and hopefully impart some wisdom along the way. I’ll be sharing links to financial websites as well as Youtube videos to help explain more complex concepts. From time to time, and for extra fun, I’ll also review a movie I believe covers a certain topic well . Join me as I navigate the financial world and share my outlook with you. From this, I hope you’ll get a bit of knowledge that helps in your daily financial life.

Okay, so far during this social distancing I’ve done a pretty decent job of staying active. How am I doing it? Well, I’ve got a smart watch/activity tracker helping me along. Not only does it track my exercise, steps, water intake, caffeine intake, sleep, and whole lot more; it also automatically reminds me to stay active.

It does this through notifications to get moving every 50 minutes of non-activity aswell as daily/weekly step tracking summaries. All this, to make sure I’m on track to live a healthy non-sedentary lifestyle!

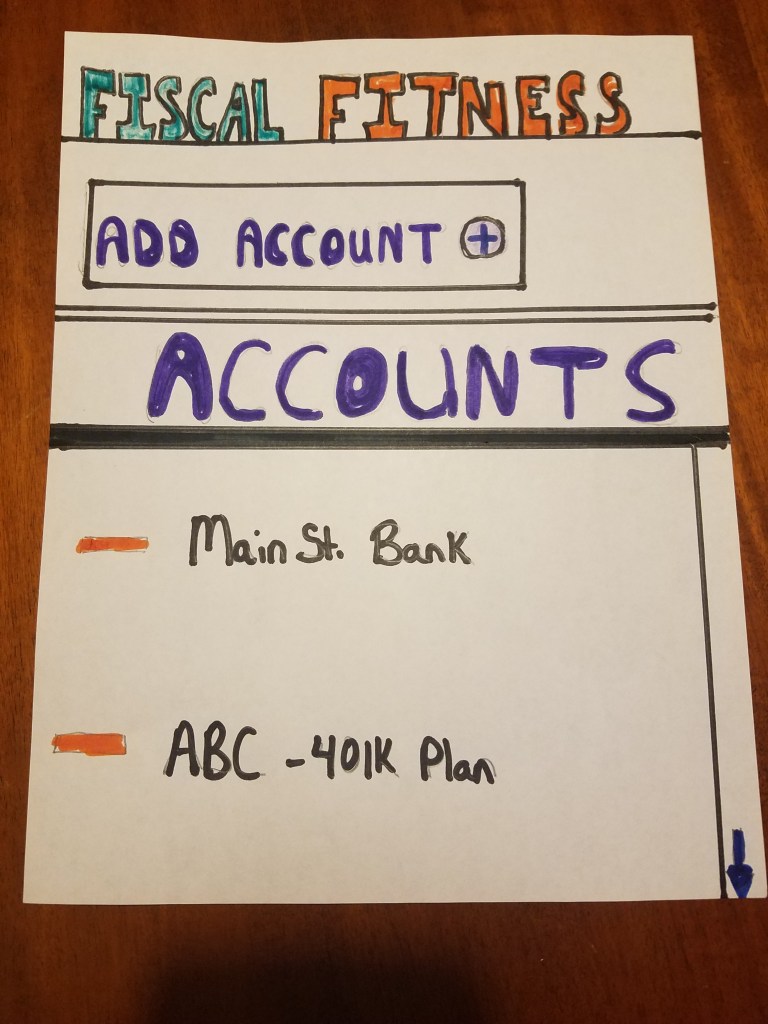

Let’s switch gears for a moment and turn our focus on financial wellness and retiring with a comfortable lifestyle. Much like my smart watch helps me with my activity my FiscalFitness app helps users stay on track financially.

The functionality of the app includes a budgeting tool that tracks weekly, monthly, and annually; a dynamic forecasting tool utilizing current income to project needed retirement assets; and an automatic investment volatility level alert.

Nobody really knows how much money they’ll need in for retirement. It’s a future number that needs to take into account several variables. One method utilized by a majority of retirement calculators, and a good rule of thumb is to assume you’ll need 70-80% of your current income.

The app will allow the user to include not only their banking and investment accounts, but also any employer retirement plan information and Social Security Benefit assumptions.

With this information the analytical forecasting tool can help the user “stay on track” to hit that retirement number. The tool is also dynamic and can update with any new information added ie – change in income, change in assumed retirement age.

Lastly, the application includes the ability to send out alerts to the user when their investment accounts hit a preset level. This level can be a loss of 10% or 15%; whatever the user wants. Once this percentage is met, an automatic notification is sent via text an email to the user who can then make adjustments to the account or call their adviser.

User will want this app as it will help set/keep budgets which in turn will help with their current financial wellness. At the same time the app will help analyze and track their path to retirement.

Times up! Gotta stay on track…my watch just reminded me to get up and stay active.

Well, here in Houston, we are still under a Stay-at-Home order. So, I’ve been doing much of what the rest of the country is doing, watching Netflix. On the menu for today – the movie “Boiler Room” and steaks. It happened to be an awesome day outside so I took advantage of the weather and decided to grill. Nothing like kicking back on the weekend with a good movie and good grub.

“Boiler Room” is told and narrated, by Seth Davis, (played by Giovanni Ribisi) a young college dropout who runs an illegal gambling game out of his apartment. It’s fairly successful, but his dad, a judge, finds out and admonishes him telling him to make an honest living.

By chance, Seth, meets an old friend who is a broker at a small brokerage firm, J.T. Marlin and is invited to interview. It’s actually a group interview lead by, Jim (played by Ben Affleck) who’s introductory monologue rivals Alec Baldwin’s, Always Be Closing speech in, “Glengarry Glen Ross.”

At J.T. Marlin, no experience is necessary. In fact, they don’t want it as they “…don’t hire brokers here — we train new ones,” Jim exclaims. This is an important point the viewer won’t be aware of until later in the movie.

As the new broker training picks up, Seth learns quickly under the mentorship of the firm’s senior brokers, Chris (played by Vin Diesel) and Greg (played by Nicky Katt). This training involves the heavy pressure sales tactics and how target “whales” to sell stocks to.

It seems almost to good to be true, as Seth learns, his firm pays much better commissions to the brokers than other larger and more established firms.

Photo from New Line Cinema

Unfortunately, the house of cards is about to take a tumble. After Seth’s curiosity gets the better of him, he uncovers the truth about the numerous stocks sold by the firm, and realizes that J.T. Marlin is no more than an elaborate ‘boiler room’ operation.

A “boiler room” a scheme in which salespeople apply high-pressure sales tactics to persuade investors to purchase securities, including speculative and fraudulent securities.

Even though Seth is no stranger to backroom scams (he used to run a highly-profitable yet illegal card game out of his home), this revelation leads to a crisis of conscience. Seth reasons that, as opposed to his previous illicit dealings, as a broker in this ‘chop shop’, he is offering his customers something they don’t want and can ill afford. Unfortunately, this is the least of his worries, as elements in law enforcement are equally aware of the truth about J.T. Marlin.

Overall, I thought it was a wonderfully paced movie. This one is in my top 5 of financial industry movies and I believe I’ve seen it over 10 ten times now. 2 Thumbs up from the my2cents guy!

As I write this, many, many people across the nation and around the global are out of work. Due the COVID-19 global pandemic and the social distancing measures enacted, jobs that required face-to-face or on-site interaction have been put on hold.

Some consequences are a layoff of work forces from companies affected by social distancing or furloughs for employees until circumstances change.

I decided to give you a glimpse into my world and how my circumstances have changed. First and foremost, though, I will say that I’m am blessed to be in the position I am and that if not for technology the situation would be different.

A couple of items to note – I work in the financial services industry and I normally have a morning commute of 1 hr 15 minutes and an evening commute of 1 and half hours.

This, as many of you may have experienced, is fairly draining on a week in week out basis. Not only do you need to wake up that much earlier to make it to work on time, but the evening is so much more compressed.

Now, my wife is an assistant principal and has to stay later after school has let out. Add in our two kids and their after school activities (dance, sports) and you get a few minutes for dinner before bedtime.

With our city and county under stay-at-home orders my company is working fully remote. So with that, my commute has been shortened greatly!

So here’s a short look at my short commute. I hope this give everyone a chuckle or two to keep their minds off the stressful events.

Video by Lindsey Summerville / Music – Prizefighter by Norma Rockwelle

Unfortunately, some of my edits were removed from the video so it’s a bit shorter than I originally made it. Oh well, it’s a good lesson to learn from even in these changing circumstances.

Wow, just….wow. What a whirlwind of events that have transpired. The confluence kicked off by the COVID-19 global pandemic lead to volatile swings in the market – both global and domestic, as well as, the massive drop in oil.

It may feel like there is nowhere to run and nowhere to hide, whether it be physical or financial health.

For the former, I’ll rely on the doctors and epidemiologists warnings and advice on preventative measures.

For the latter, I’d like to introduce a financial vehicle I might have mentioned in the past, but many people my not be familiar with – the annuity.

Photo by Lindsey Summerville

Over the past weeks and months investors are most likely wondering what to do. Should I stay in stocks? What if they keep going down? Should I move to bonds? The yields are really low and if rates rise the value of the bonds will go down.

Enter, the Fixed Indexed Annuity. This is a product that is not an investment, it is a contract with an insurance company that will credit interest to a policy, depending on the performance of the index it is linked to.

That might be a little wordy, but simplistically the Fixed Indexed Annuity does the following:

Protects the principal – you can’t lose money due to the volatility of the market/index. If you put $100,000 in, that is protected even if the index the policy is linked has a negative return.

Provides accumulation potential – the policy is linked to a market index and interest is credit with positive index performance. Each interest credit is calculated with the previous balance, compounding the benefit.

Lifetime income – depending on the product, a guaranteed lifetime income stream can be provided either through a provision called an income rider or through annuitization

Tax Deferral – earnings grow tax deferred

The Fixed Indexed Annuity is not a substitute for stocks. It’s not designed to have performance similar to the S&P 500 for instance.

Generally, an FIA, can be seen/used as a bond alternative. An option for safe accumulation with returns between 3% – 7% overtime.

You might be asking, okay, what’s the catch. Well, in order for the products to work as designed, there are holding periods or surrender schedules where a fee is paid if you take the money out. For instance, if you are in a 7yr product and want to take all your money out in the 1st year, you might have to pay a 7% penalty. In year 2, the penalty could slide down to 6%, in year 5 it could slide down to 5% and so on.

Most products allow for a free withdrawal up to 10% of the account value before any surrender charges are incurred though.

Overall, if an investor is looking for protection from market volatility, an annuity can offer safe accumulation as well as lifetime income.

Below are two places to get additional information on the basics of fixed indexed annuities.

After writing a few recent post I got to thinking. There may be certain facets of the financial industry people hear about on the news each day, but don’t really know what they are.

I’ve decided to start a new series, Back to the Basics, where I’ll cover a few items at a time and explain just what they are, how they’re used, or where they came from.

For starters, how about the a bull market and a bear market. Well, according to investopedia they are defined as follows:

A bull market is the condition of a financial market in which prices are rising or are expected to rise.

You may be asking why the names bull and bear though. Well, there are many theories of the origin, but the one most of cited is the way they attack their prey. Bears come down while bulls gore up!

Charging bull sometimes referred to as the Wall Street Bull

The New York Stock Exchange. The Dow Jones Industrial Average Index is tracked here.

GM common stock certificate.

Dow Jones. I know you’ve heard this countless times, but what is it? Well, it’s actually short for the Dow Jones Industrial Average which is an index that tracks 30 large, publicly traded companies on the New York Stock Exchange. It’s name after, Charles Dow, who created it along with his partner Edward Jones, in 1896.

Why is it important? It’s made up of blue chip companies and was designed to be seen as representative of the shape of broader U.S. economy. It’s evolved over time in composition and only had 12 companies originally.

So you want to buy some stock! That means you want to make an investment that represents an ownership share in a company. You do this in the hopes that the company will do well and thus the price of that share will rise. If you sell it for more than you paid for it you will have made a profit. However, stock prices don’t always go up. Sometimes they go down and if you sell for less than you paid then you will have a loss. Pretty straightforward, but there are other facets that can get pretty complicated. We’ll save that for next time though!

In my first blog post I mentioned that I would be reviewing movies for some fun and a change of pace. As we move ever deeper into the COVID-19 pandemic and markets tumble, now’s a good a time as any to take a look at the movie, The Big Short.

The Big Short Trailer

The Big Short, is a 2015 Oscar-winning movie that follows multiple characters whose stories all have one thing in common, they see major problem in the U.S. housing market. The film chronicles the…. and the events leading up to the global financial crisis.

It’s a movie heavily steeped in financial industry jargon and strategy. To help with this, the director and screenplay incorporate a short vignette with exposition delivered directly to the audience via celebrity monologue. The helps the laymen make sense of who’s done what and how.

The plot’s starting parting point begins with, Michael Burry, a seemingly austistic-potrayed hedge fund manager who has discovered the U.S. housing market is extremely unstable. This market is based on ‘subprime loans’ of high risk (although the bonds they are packaged in are highly rated – meaning low risk). He predicts the market to collapse around 2007 and looks to profit from the drop. He develops a short-selling strategy (a bet against the prevailing market sentiment) that catches the attention of Jared Vennett.

Vennett, is a stockbroker looking to get out of his position, that the housing market will do well, and seeks others to take up on his new found strategy.

Another hedge fund manager, Mark Baum, hears Vennett out and decides he will short the housing market as well. This is done through and arrangement called a credit default swap. As Mark learns more and more about the mortgages that have been bundled to together to form the bonds the banks are selling as investments, he finds out that they’ve been packaged and resold

Photograph: Everett/Rex shutterstock

The film also includes a final set of characters that figure of the impending collapse, Charlie Geller and Jamie Shipley. These two young investors look for guidance from retired investment banker, Ben Rickert, after finding a white paper written by Vennett.

Ultimately, the housing market falls thus triggering the global financial crisis. Multiple investment banks declared bankruptcy, millions of people became homeless, lost their jobs, and trillions of dollars were wiped away.

I highly recommend this movie as it’s very informative on a subject matter that you may have heard about but better never really knew about.

Wow, oh, wow! What a week it’s been in the markets – both domestically and globally. I’m sure you’ve been paying attention, but if you haven’t, there has a been a massive amount of fear-induced selling due to the novel Coronavirus.

In fact there has been so much selling that Dow Jones Industrial average, S&P 500, and the NASDAQ Composite all had their worst weeks since the global financial crisis in 2008.

Each of those indices is now in correction territory, meaning there’s been a loss of at least 10% from their respective highs. Corrections are not uncommon as they happen on average every 8 to 12 months. If selling continues, however, and markets go down 20% below the all-time highs, that is called a bear market.

So what happens next? Well, we’ll see. A lot depends on the progression or containment of the coronavirus, along with the timeline of vaccine development.

This most likely won’t be resolved in a few weeks though so if the disease spreads even more, a disruption in supply chains will have a heavy impact. As one domino falling affects the next, the shut down of industry and production in one part of the world can affect end users and buyers in another.

A global ripple, left unchecked, could develop into a recession. A recession is a period of declining economic performance across an entire economy, frequently measured as two consecutive quarters.

It’s the beginning of February and just around the corner, at least here in Houston, it will be time to plant seeds for summer vegetables. The growing seasons awaits. In my garden I usually grow tomatoes, cucumbers, green beans, okra, onions, and peppers. I call myself a goat because I’ll eat pretty much everything, my kids however, not so much.

I aim to plant around March 1, just about the earliest time possible in order to maximize the growth and yield when it’s harvest time (or it get’s too unbearably hot – for both the plants and myself). If I wait too long to plant I may not give the seeds a long enough to time germinate, sprout, flower and bear fruit. I want the best chance at enjoying the fruits of my labor.

Photo by Lindsey Summerville

Similarly, when saving for retirement, you want to give yourself the best chance to enjoy the fruits of your career labor. How’s that? Start early!!!!!!!

An investor can always increase the amount they set aside (save/invest). An investor can always increase the frequency or how often they set aside (save/invest)money. However, a saver/investor cannot increase the amount of time. Perhaps, you can postpone retirement, you say. Well in those years closest to retirement, you’ll want to be transitioning towards investments that have a lower risk/reward profile. In order to make up for lost time you may risk losing some of the assets you worked so long for.

Check out this article on investing as early as possible. Neat infographic included!

So plant those seeds for financial success early: set aside your pizza and beer money, invest in your company’s retirement plan, make a budget, stick to the budget, do what you can even if it’s a little!

Photo by Lindsey Summerville

“Do not save what is left after spending; spend what is left after saving.” – Warren Buffett

New yield? Yes, but not in a good way. I wrote this post last Monday when the U.S. 10- year Treasury closed with a rate of just 1.52%. One year earlier, it closed at 2.72% What exactly does this mean and what impact does it have?

For starters, a 10-year Treasury note is a loan made to the U.S. Government. Think of it like a person getting a loan from the bank, but in reverse. For loaning this money the purchaser in return will receive a fixed rate of interest. 10-year Treasury notes are considered an extremely safe investment due to backing of the full faith and credit power of the government.

Photo by Lindsey Summerville

The notes are purchased at initial auction or on the secondary market and sold to the highest bidder. This happens daily. When investors are looking for safety and the notes are in high demand they may be sold at higher than face value. This reduces the overall the Yield of the investment.

What affect does that have on you? I can be both good and bad at the same time. 10-year Treasury note yield is a benchmark for other interest rates. If the yield goes up, the interest rates on 10 and 15 year fixed rate mortgages do as well. This means if you decide to buy a home and get a loan, you would end up paying a higher rate to borrow that money. If rates are lower then you would be paying less.

However, if the 10-year Treasury note is low, other investment that may be less safe can also fall and remain competitive.

Lastly, the 10-year Treasury rate compared with other rates can be an indicator of sentiment on the economy. If investors aren’t confident, they will seek safety. As the 10-year treasury is virtually risk-free, a higher demand will drive down the rate.

This means investors are less confident in the economy now than they were a year ago.

“Our greatest glory is not in never failing, but in rising every time we fall.”

Recently you may have heard that Congress passed the SECURE Act. What is it? Well Congress loves their acronyms, so stay with me here. It’s the Setting Every Community Up for Retirement Enhancement Act of 2019. Clever huh?

The bill aims to increase the access to tax-advantaged accounts and preventing older Americans from outliving their assets.

To do this certain existing rules were relaxed to encourage employers that don’t currently have retirement plans to start one. Others allow retired individuals to delay required distributions from their qualified accounts.

One such rule for employers allows businesses to sign-up part-time employees who work either 1,000 hours through out the year or have three consecutive years with 500 hours of service.